A STOCK Act for the Third Branch

Congress included the Supreme Court and lower federal courts in a 1978 law that requires top federal officials to file annual financial disclosure reports. But the judiciary was mostly[1] left out of the 2012 STOCK Act and the 2013 revision.

Congress included the Supreme Court and lower federal courts in a 1978 law that requires top federal officials to file annual financial disclosure reports. But the judiciary was mostly[1] left out of the 2012 STOCK Act and the 2013 revision.

The Supreme Court was left out completely.

The operative part of the 2012 statute states that senior officeholders in the legislative and executive branches must publicly disclose their securities transactions within 45 days.

The goal is to ensure that federal officials aren’t profiting off insider information gleaned from their jobs.

Contrast that to the judiciary today. If a Supreme Court justice or other federal judge were to buy Amazon shares on Dec. 31 of a given year, the public could only expect to learn about it at the earliest on the next June 15, or 167 days later – a wait four times longer than of those covered by the STOCK Act.

Had the justice bought the shares on Jan. 1, the public could not expect to learn about the purchase until June 15 of the following year, or 531 days later – a delay by a factor of 12. In fact, Chief Justice Roberts’ Jan. 5, 2016, sale of his Microsoft shares wasn’t confirmed until the 2017 SCOTUS disclosures were released 520 days later[2]. A wait this long means a case involving the company easily could have ended in the interim, and a missed recusal, which may have altered the outcome, has gone unheeded.

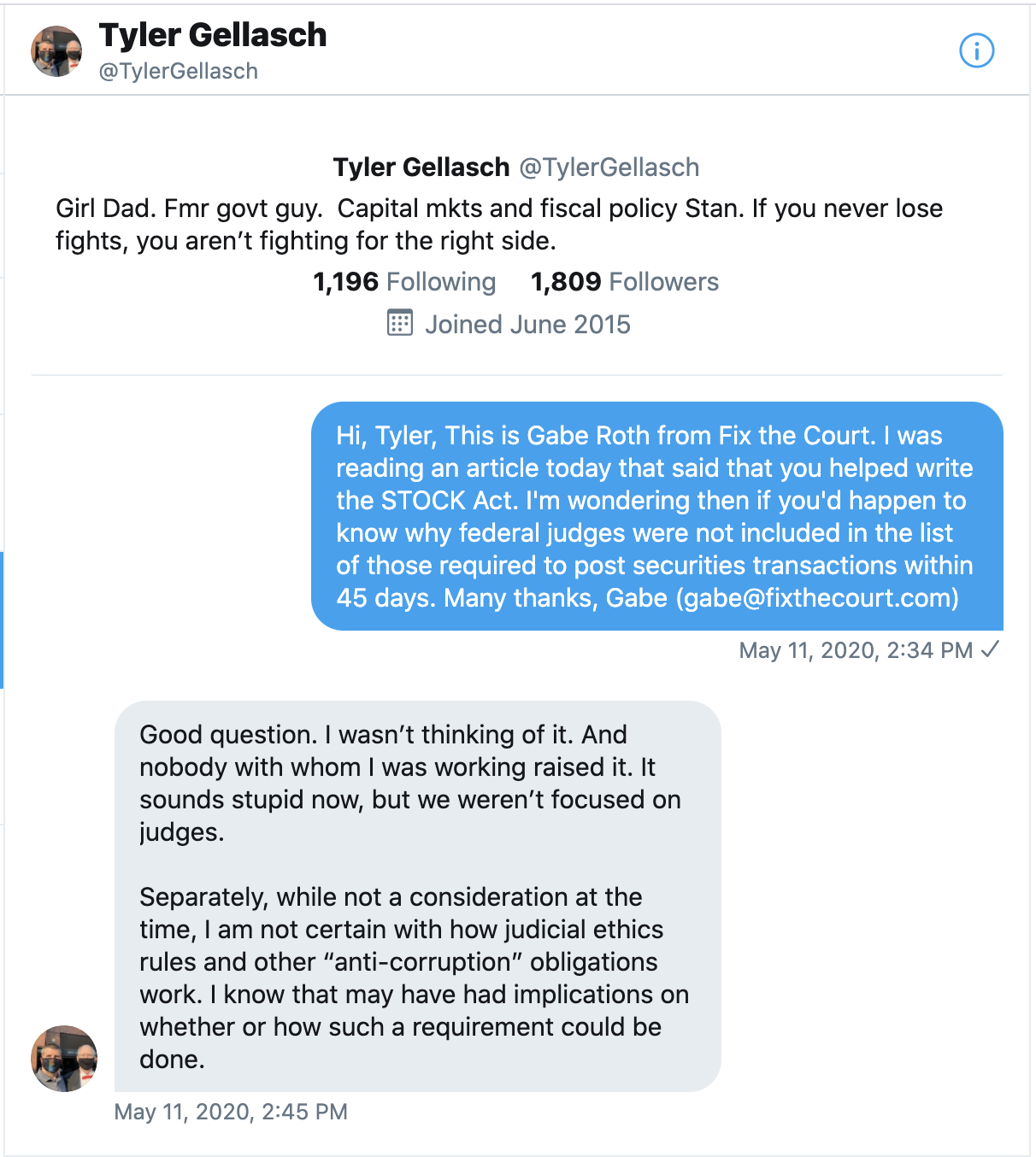

The omission of the judiciary from the 45-day rubric did occur not for any discrete reason – “I wasn’t thinking of it, and nobody with whom I was working raised it,” according to the congressional aide who spearheaded the bill – but was due to its provenance being a response to a “60 Minutes” story on stock trades by members of Congress.

{kind=link}

By our estimates, 30 to 40 percent of federal judges own shares of individual stock; the rest solely hold blended or index funds, bonds or retirement accounts, which are unlikely to yield statutory financial conflicts. Further, we know that every year, members of the former group – stock-owning judges and justices – sit on cases despite a financial conflict, sometimes willfully, though often inadvertently.

That’s not only illegal – a judge may not participate in a case if he or she “has a financial interest in the subject matter in controversy or in a party to the proceeding” – but it also degrades public faith in the third branch.

A more immediate public accounting of judges’ and justices’ securities transactions – a Judiciary STOCK Act with a 45-day reporting requirement – would provide assurance of the propriety of these transactions and would encourage judges to better familiarize themselves with their portfolios, take financial conflicts more seriously and be more proactive about disqualifying themselves when required by law.

Case Study No. 1: Lower Court Judges Caught by The Center for Public Integrity

In 2014, the Center for Public Integrity obtained the 2010-2012 financial disclosure reports filed by all but three of the 258 judges who sit on federal appeals courts. In all, CPI identified 24 cases where judges owned stock in a company with a case before them and didn’t recuse.

Here’s one example: Linda Wolicki-Gables took her case against Johnson & Johnson over a malfunctioning internal medication pump to the Eleventh Circuit in 2011 and years later learned that one of the judges on the panel that ruled against her, Judge James Hill, owned as much as $100,000 in the company’s stock. The malfunction has left Wolicki-Gables a partial paraplegic. CPI found that Hill ruled on three other cases involving companies in which he owned stock, and “in all four instances, the court rulings favored his financial interest.” The story continues:

“The Center’s findings point to a larger issue of accountability – or lack thereof – in the federal court system. Judges face no formal punishment for breaking these rules.

“Appellate judges can affect a company’s stock price – or even an entire industry sector – with their rulings. They are also far more likely to own stock than the average American, making it all the more important for them to avoid the perception that their holdings could influence their rulings.”

A new STOCK Act that includes federal judges and justices would add an important layer of accountability that is sorely lacking in the third branch – one that would have negligible costs but far-reaching benefits.

Case Study No. 2: Fix the Court Tracks SCOTUS Missed Recusals Due to Stock Ownership

Seemingly every term, a Supreme Court justice fails to recuse from a case or petition due to stock ownership. In 2015, FTC asked the three stock-owning justices – Chief Justice John Roberts, Justice Stephen Breyer and Justice Samuel Alito – to sell their shares of stock, and they’ve since responded by reducing the number of companies whose shares they own by half. Nevertheless, the three still collectively own shares in three dozen companies and continue to make unforced errors related to those holdings. For example:

On Jan. 14, 2019, Breyer and Alito failed to recuse in Feng v. Komenda and Rockwell Collins, Inc., despite both owning shares in Rockwell’s parent company, United Technologies Corp. After FTC brough this missed recusal to the Court’s attention, the justices responded that they’d have had “no way” to know about the conflict since the company in question waived the right to respond. FTC finds that reasoning specious.

On June 18, 2018, Roberts failed to recuse in Marcus Roberts et al. v. AT&T Mobility despite owning shares in Time-Warner, which had merged with AT&T four days prior.

On June 27, 2017, Alito failed to recuse in Merck Sharp & Dohme Corp. v. Albrecht despite owning shares in Merck. He eventually disqualified himself, albeit three months later.

On Dec. 6, 2016, Roberts failed to recuse in Life Technologies Corp. v. Promega Corp. despite owning shares in Thermo Fisher Scientific, which owns Life Technologies. Robert did recuse the following month.

On Oct. 14, 2015, Breyer failed to recuse in FERC v. EPSA despite owning shares in Johnson Controls, a party on the EPSA side. Breyer learned about the conflict the day after oral argument, Oct. 15, and sold his stock that day, after which he remained on the case, which is permitted by federal law but ethically questionable.

On Oct. 5, 2015, Roberts failed to recuse in ABB Inc., et al. v. Arizona Board of Regents, et al., despite owning shares in Texas Instruments stock, a party on the ABB side. Even after FTC brought this to the Chief’s attention in Dec. 2015, no further action was taken, and Roberts to this day owns shares in Texas Instruments.

————–

[1] Section 9 of the Act states, “The Judicial Conference shall issue guidance for federal judges and judicial employees regarding the prohibition of use of nonpublic information derived from a government job to make a private profit.” Note that this guidance does not include Supreme Court justices, nor is it available online for members.

[2] This reporting lag is often longer for federal judges not on the Supreme Court. Due to an ongoing staffing shortage in the U.S. Courts’ Financial Disclosure Office, zero circuit and district judges’ 2019 disclosures, which were due by law on May 15, 2020, have been released to the public, and only half of the judiciary’s 2018 disclosures, due by law on May 15, 2019, have been released, 471 days ago and counting.